Retirement planning is not just about saving up money. It is also about making sure that your accumulated wealth will keep up with the cost of living when you are no longer working. Most people focus on building up a large corpus, but what they often overlook is inflation. Prices are always going up, and that means a retirement goal that looks solid today can turn out to be woefully inadequate a few years down the line.

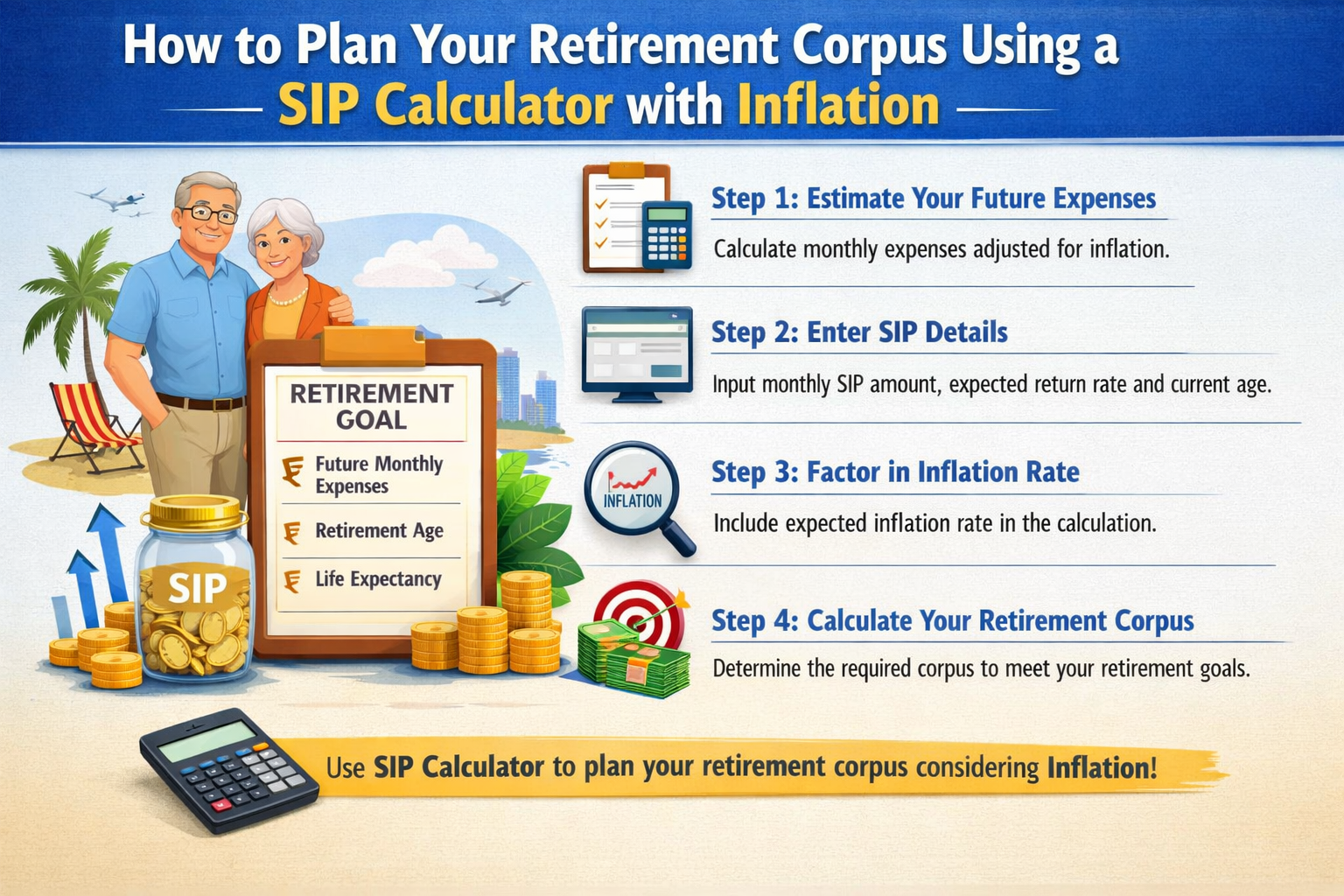

To get a grip on your retirement planning, you need a tool that can factor in both the compounding effect and the rising costs of everyday life. This is where a SIP calculator that includes inflation assumptions is a total game-changer.

It helps you turn today’s savings into a real picture of what you can actually afford in the future, making the whole planning process way more realistic and manageable.

Why You Can’t Afford to Ignore Inflation

Inflation gradually chips away the value of your money. Expenses like healthcare, housing, and daily living tend to keep on going up. In fact, even a relatively modest inflation rate can do some serious long-term damage to your financial situation.

Think about this for a second: A monthly expense of 50,000 rupees today may be a lot bigger 20 to 25 years from now. And if you are not accounting for that extra growth in your retirement planning, you may end up way off the mark.

By factoring in inflation, you can get a better handle on what your future expenses are really going to be, rather than just pretending they are the same as they are now.

Role of SIP in Building a Retirement Corpus

Investing regularly can turn long-term goals into something that feels manageable, even in the face of big changes in your life (like retirement).

It is a lot easier to save for the future when you break it down into smaller, monthly chunks. That is where SIPs come in; they let you build up your wealth incrementally, rather than having to find a huge sum of money all at once.

Using SIP for retirement plans helps you stay organised and benefit from the compounding effect. By making a regular contribution, you avoid the stress of trying to time the markets and make investing something that is more of a habit.

How a SIP Calculator with Inflation Helps

A SIP calculator with inflation is a powerful tool because it looks at different variables in one place. It considers things like what you expect to earn on your investment, how much you can invest each month, and how inflation is going to affect your money.

This helps answer some really important questions:

- How much do I need to invest each month if I want to hit my target savings goal?

- How much of an impact will inflation have on my savings?

- What happens if I decide to invest more money into my investments over time?

By seeing all these possible outcomes along with the expected rate of inflation laid out in front of you, you get a clear idea of whether your current savings strategy is on track or needs a bit of tweaking.

One key takeaway from inflation-adjusted planning is that sticking to fixed contributions just isn’t enough. As you earn a higher income over time, you really need to be topping up your investments.

Because of inflation, the value of your money is actually going down every year, so your investment amounts should ideally be going up too. Making regular increases to your SIP contributions can really help bridge that gap inflation creates.

Final Thoughts

Retirement planning must consider how inflation is going to affect your future expenses.

A retirement plan using SIPs and inflation-adjusted calculations is a good approach, and it can help you turn long-term goals into actual, achievable steps.

By starting early, gradually investing more money in and being realistic about inflation, you can create a retirement corpus that will give you the financial security you need and also the freedom to live the life you want.

{kind=link}